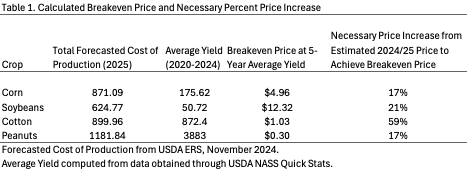

On Monday, January 12, 2026, the USDA World Agricultural Supply and Demand Estimates (WASDE) report was released with some unexpected projections. A record corn crop is even larger than expected, now projected at 17 billion bushels, up 269 million bushels from the prior month. This is a result of a record yield of 186.5 bushels per acre on a record 91.3 million harvested acres. While total use was also increased to 16.4 billion bushels, the stocks-to-use ratio is projected to be 13.6%, up from 12.5% a month earlier, and up from 10.3% compared to 2024/25.

It’s been well documented in previous Southern Ag Today articles that the stocks-to-use ratio is a good predictor of corn marketing year average prices. Thus, the increase in the ratio is expected to result in a decrease in price. In fact, the corn futures market responded with an immediate sharp decline on Monday. The pre-report price of the March corn futures was $4.474/bu, which by close ended the day down 26 cents at $4.214/bu. As a result, most of the gains that had accrued in this contract since the low price of $4.122 was projected on August 12, 2025, have since been returned. The USDA did raise the marketing year price projections for 2025/26 to $4.10, although this is still down 14 cents from the 2024/25 price of $4.24.

Soybean prices were also affected by the WASDE release, with March soybean futures falling 20.2 cents from a pre-WASDE release price of $10.692/bu to $10.49/bu at close. This was on news that soybean supply for 2025/26 is 17 million bushels higher than estimated in December. Yield remained at a record 53 bushels per acre, but harvested acres increased to 80.4 million, resulting in about 9 million bushels of additional production. Beginning stocks for 2025/26 were also adjusted up about 9 million bushels since the prior month estimates. On top of supply increases, total use dropped 43 million bushels, driven largely by a 60 million bushel drop in exports due to higher production and competition from Brazil. The resulting stocks-to-use ratio increased to 8.2% for 2025/26, up from the 6.7% projected in December. The USDA also adjusted the 2025/26 marketing year average price estimate down 30 cents to $10.20/bu.

All was not completely bearish for southern agriculture, though, as Cotton markets remained stable with March futures contracts staying just under $0.65/lb. The WASDE report showed a lower expected yield of 856 lbs/acre on 7.8 million harvested acres. This reduced production estimates to 13.92 million bales. Meanwhile, total use was stable at 13.8 million bales. The USDA now projects the 2025/26 marketing year average price for upland cotton at $0.61/lb. The challenge for producers is that this report does not make planting decisions and marketing for 2026 any easier. With a solid marketing plan, it’s best to avoid reactionary decisions to market movers like this and focus on executing the existing plan (see https://southernagtoday.org/2026/01/07/a-new-year-a-better-marketing-plan-for-the-farm/), which should account for the ups and downs in commodity markets.

Rabinowitz, Adam. “Surprise! January WASDE Report Moves Corn and Soybeans Lower – Cotton Flat.” Southern Ag Today 6(3.3). January 14, 2026. Permalink