Low commodity prices, high input costs, and trade market uncertainty have placed significant financial strain on many row crop producers throughout the U.S. In response, the U.S. Department of Agriculture developed the Farmer Bridge Assistance (FBA) program (USDA-FSA, 2025a). The FBA program aims to deliver one-time commodity-specific payments ($/acre) to row crop producers to serve as a financial bridge until the benefits of the One Big Beautiful Bill Act (OBBBA) become available in October 2026 (USDA-FSA, 2025b). Payments will be made to eligible producers based on 2025 planted acres reported to the FSA. Farmers who qualify for the FBA program can expect payments to be released by February 28, 2026 (USDA-FSA, 2025a). On December 31, 2025, the USDA released details on the per-acre payment rates for all eligible row crop commodities (USDA-FSA, 2025b). Rice farmers who qualify for the FBA program will receive a payment rate of $132.89/acre.

This article evaluates the impact of the FBA Program on rice returns to operating and total (operating plus fixed) costs in the southern U.S. The analysis is based on average rice production costs and average expected rice yields obtained from 2025 Cooperative Extension rice enterprise budgets from Arkansas, Louisiana, Mississippi, Missouri, and Texas. Seven southern U.S. rice regions are evaluated (Eastern Arkansas, Mississippi Delta, Southeast Missouri, Northeast Louisiana, Southwest Louisiana, Texas Gulf East, and Texas Gulf West). Results for Southwest Louisiana and Texas Gulf West are evaluated for the first crop and for the first crop plus a ratoon crop. Average rice yields, costs, and returns per acre for the analysis are presented below in the accompanying table.

Figure 1 presents budgeted rice returns to both operating costs and total costs by southern U.S. rice region without assistance from the FBA program. Budgeted returns to both operating costs and total costs are negative for all regions except those located in Louisiana. Operating costs in the Louisiana rice regions are lower due to lower herbicide, fertilizer, and seed costs.

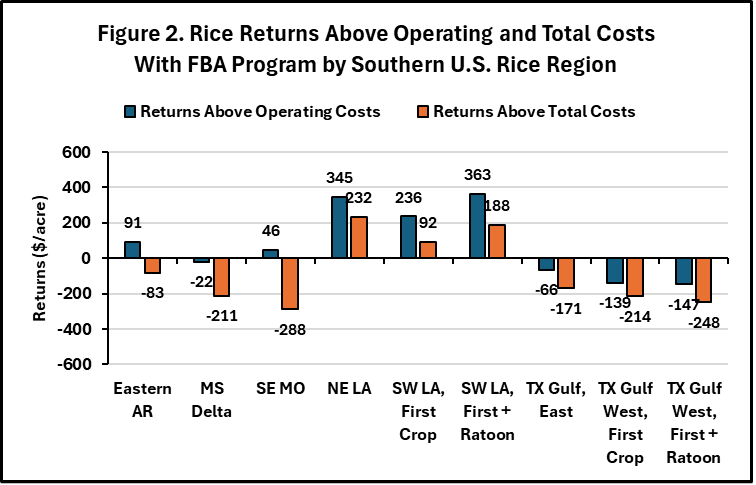

Figure 2 presents rice returns to both operating costs and total costs by southern U.S. rice region when assistance from the FBA program is included. Returns to total costs by region are still largely negative except for the Louisiana regions. However, returns to operating costs are either positive or close to breakeven for many of the remaining southern rice regions.

It is important to note that these results are from pre-season budget estimates not actual 2025 observations, but they do provide an estimated scope of the FBA program impact in rice. Results indicate the FBA program may not help with covering total costs in most instances, but would aid in covering most or all of rice operating costs. Thus, the FBA program could help many rice producers obtain operating loans for production inputs, thus allowing them to get a rice crop planted for the 2026 crop year.

Table 1. Average Rice Yields, Costs, and Returns by Southern U.S. Rice Region based on State Cooperative Extension Rice Enterprise Budgets, 2025

| Region | Yield (cwt/acre) | Operating Costs ($/acre) | Total Costs ($/acre) | Gross Returns ($/acre) | Returns Above Operating Costs ($/acre) | Returns Above Total Costs ($/acre) |

| Eastern AR | 81 | 947 | 1121 | 905 | -42 | -216 |

| MS Delta | 76 | 1006 | 1195 | 851 | -155 | -344 |

| SE MO | 78 | 953 | 1286 | 865 | -87 | -420 |

| NE LA | 73 | 597 | 710 | 810 | 213 | 100 |

| SW LA, First Crop | 72 | 701 | 845 | 804 | 103 | -41 |

| SW LA, First + Ratoon | 98 | 859 | 1034 | 1089 | 230 | 55 |

| TX Gulf, East | 55 | 813 | 918 | 614 | -199 | -304 |

| TX Gulf West, First Crop | 70 | 1054 | 1129 | 782 | -272 | -347 |

| TX Gulf West, First + Ratoon | 86 | 1241 | 1341 | 960 | -280 | -381 |

| Note: Gross returns calculated assuming an average long grain rice price of $11.17/cwt for the months of August – October 2025 (USDA, NASS, 2026). Total costs are calculated as operating plus fixed costs and exclude charges for land and management. | ||||||

References and Resources

Louisiana State University AgCenter. LSU College of Agriculture. Enterprise Budgets. https://www.lsuagcenter.com/portals/our_offices/research_stations/deanlee/features/enterprise-budgets

Mississippi State University, Department of Agricultural Economics. Budgets. https://www.agecon.msstate.edu/whatwedo/budgets.php

Texas A&M Agrilife Extension, Extension Agricultural Economics. Texas Crop and Livestock Budgets. https://agecoext.tamu.edu/resources/crop-livestock-budgets/

University of Arkansas System Division of Agriculture, Cooperative Extension Service. Crop Enterprise Budgets for Arkansas. https://uaex.uada.edu/farm-ranch/economics-marketing/farm-planning/budgets/crop-budgets.aspx

University of Missouri Extension. Missouri Crop and Livestock Enterprise Budgets. https://extension.missouri.edu/programs/agricultural-business-and-policy-extension/missouri-crop-and-livestock-enterprise-budgets

USDA-FSA, 2025a. Farmer Bridge Assistance (FBA) Program. https://www.fsa.usda.gov/tools/informational/fact-sheets/farmer-bridge-assistance-program

USDA-FSA, 2025b. USDA Announces Commodity Payment Rates for Farmer Bridge Assistance Program. December 31, 2025. https://www.fsa.usda.gov/news-events/news/12-31-2025/usda-announces-commodity-payment-rates-farmer-bridge-assistance-program

USDA-NASS (2026). United States Department of Agriculture, Quick-Stats. https://quickstats.nass.usda.gov/

Watkins, Brad. “Potential Impact of the Farmer Bridge Assistance Program on Southern U.S. Rice.“ Southern Ag Today 6(4.1). January 19, 2026. Permalink