Authors Josh Maples and David Anderson

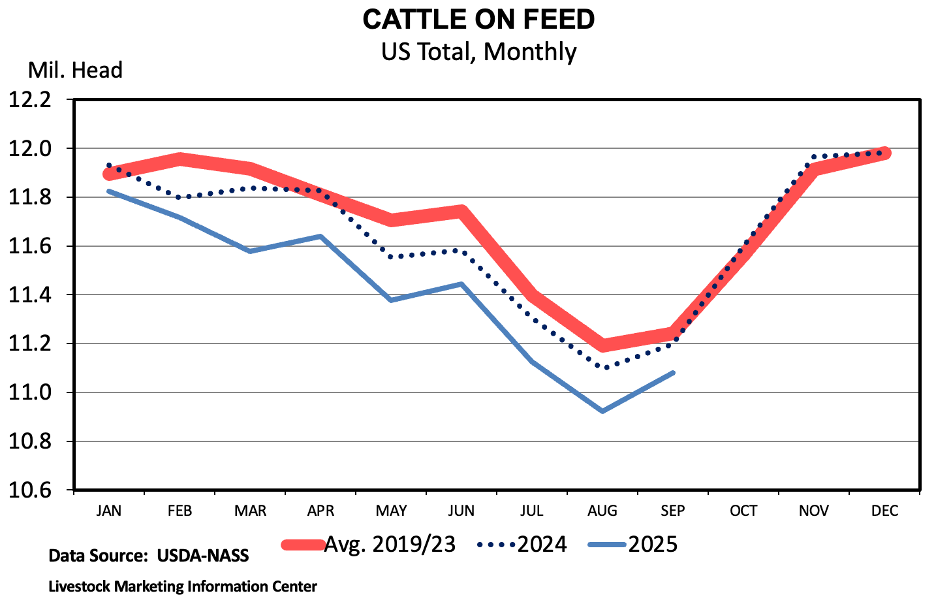

For the many industry watchers who have long wondered how much bigger cattle slaughter weights could get, the latest trends suggest 2026 could see weights continue to rise. Steer dressed weights averaged 984 pounds during the second week of February. Assuming a 62.5 percent dressing percentage, that implies an average live steer weight of 1,575 lbs. As shown in the chart, this is up from a year ago and also up from earlier years.

Federally inspected slaughter has been trending lower due to tight supplies of cattle. For the first two months of 2026, total cattle slaughter is 7.3 percent below the same period of 2025, which includes an 8.6 percent decline in steers, a 6.9 percent decline in heifers, and a 17 percent decline in beef cows. Only dairy cow slaughter is up (6.9 percent) from a year ago. Due to heavier weights, beef production this year is only down 5.5 percent compared to the same period last year. The current market is defined by two clear themes of heavier weights and fewer cattle.

Seasonally, we’d expect steer weights to decline during the first half of the year, but that has not yet happened. Dressed weights are well above the 2020–2024 average and continue to trend higher at a time when they would normally be easing. Despite the strong prices, cattle are staying on feed longer. In the current environment of strong fed cattle prices and relatively manageable cost of gain, feedlots appear willing to add pounds rather than market cattle lighter. Packers need cattle but have not broadly begun to pull cattle through faster in a way that would lead to declining average weights. The winter storm in late January does not appear to have impacted dressed weights either.

As we move further into the year, the key question will be if/when weights will break seasonally. For now, cattle dressed weights are historically high, slaughter is lower, and overall supplies remain very tight.

Maples, Josh, and David Anderson. “Heavy Cattle Weights and Fewer Head.” Southern Ag Today 6(10.2). March 3, 2026. Permalink