Authors: [1]Luis Ribera, Texas A&M AgriLife Extension Service

Aleks Schaefer, Oklahoma State University

To say that it has been a very busy year for U.S. agricultural trade is an understatement. Since “Liberation Day” back on April 1, 2025, and even before that, trade has been a major news topic. The current administration’s strategy of leveraging tariffs (combined with the sheer size of the U.S. market) to change trade relationships with the rest of the world has generated much uncertainty in nearly all markets. Both agricultural and non-agricultural industries have reacted to the almost daily trade talk news.

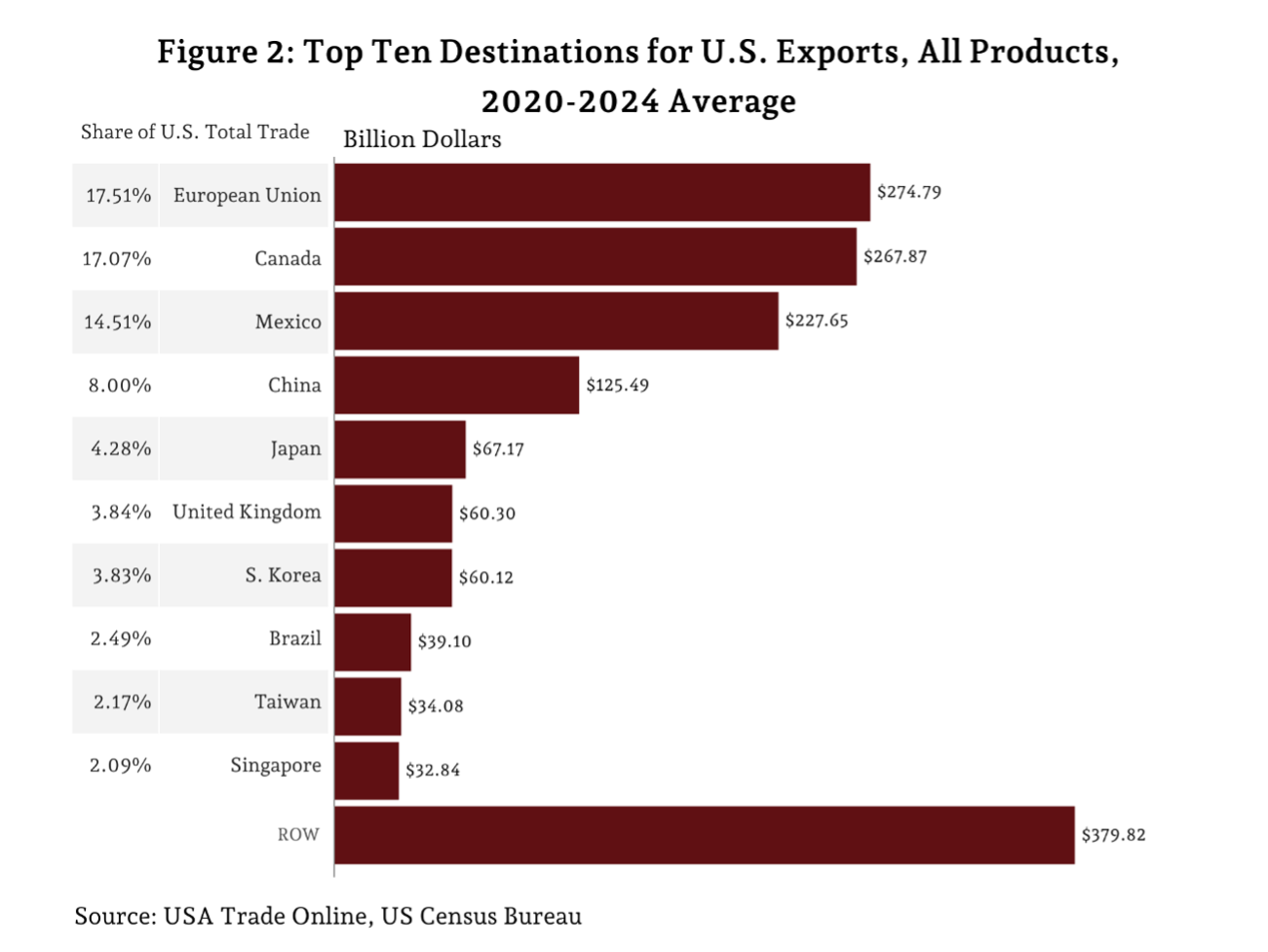

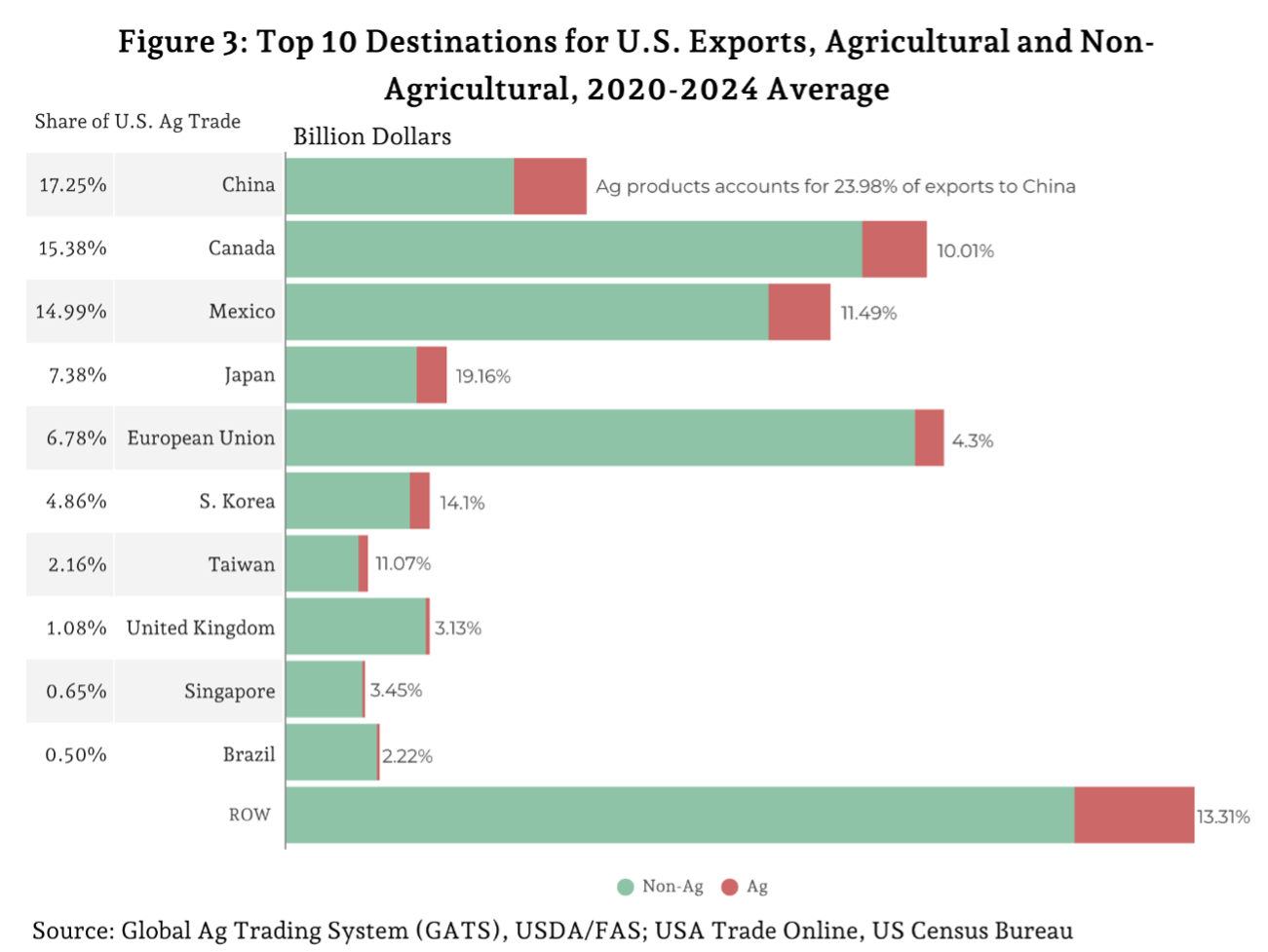

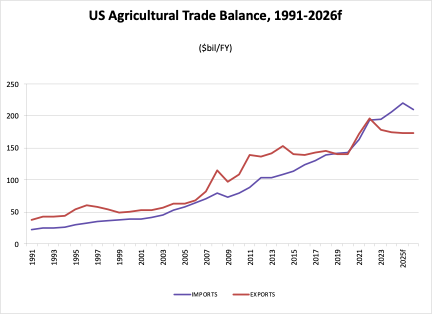

U.S. agricultural exports wrapped up 2024 at $174.1 billion. USDA Outlook for U.S. Agricultural Trade December 2025 report forecast that exports will close 2025 slightly higher than the previous year at $175.6 billion. However, the forecast for 2026 exports is $173 billion, the lowest since 2021. The reason for this slight decrease is both volume and value, as they are expected to decrease by 1.1% and 1.5%, respectively. A continuous decrease in soybean and sorghum exports to China are the main driver of the decrease in value of U.S. ag exports in 2025, as well as expectations for 2026. China increased their imports of these two products from Brazil and Argentina due to the increased of U.S. tariffs on their exports. There has been an increase in exports to other countries such as the EU, Mexico, Indonesia, and Vietnam, but not enough to offset the decrease in exports to China.

On the other hand, U.S. agricultural imports are expected to reach an all-time high in 2025 at $219.4 billion and are expected to decrease in 2026 to $210 billion. The main reasons for this expected decrease are lower imports of horticultural products and vegetable oils. Cocoa and products, as well as coffee and products, have increased the value of imports but reduced the volume, showing that prices of those products are expected to go up. Hopefully, the recent announcement of tariff exceptions on some agricultural products, including beef, tea and coffee, fruit juice, cocoa, spices, bananas, oranges, tomatoes, and certain fertilizers, will help reduce their prices paid by U.S. consumers.

[1] Ribera is Professor, Department of Agricultural Economics, Texas A&M AgriLife Extension. Schaefer is Associate Professor, Department of Agricultural Economics, Oklahoma State University.