Authors

Ryan Loy, Assistant Professor, University of Arkansas

Alvaro Durand-Morat, Associate Professor, University of Arkansas

2025 Domestic Market Recap and 2026 Outlook

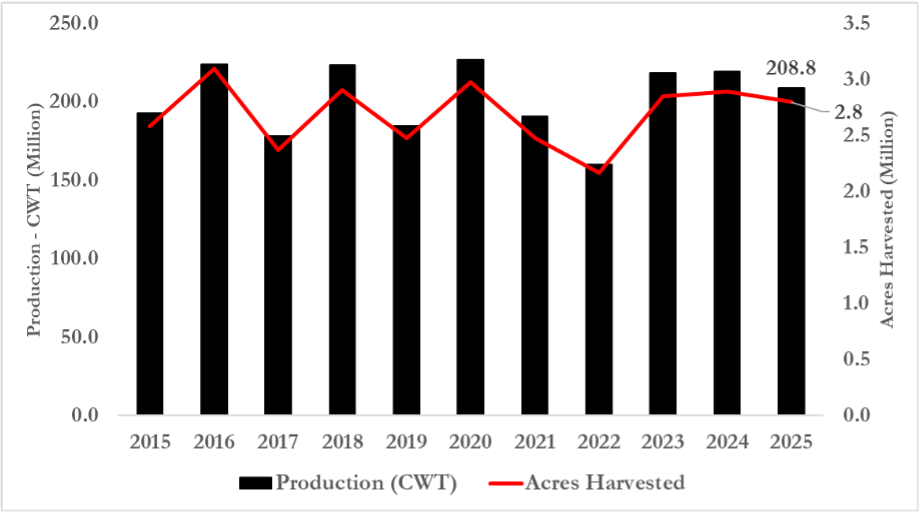

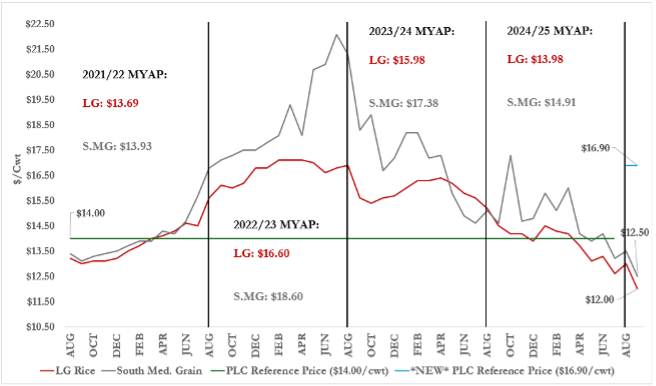

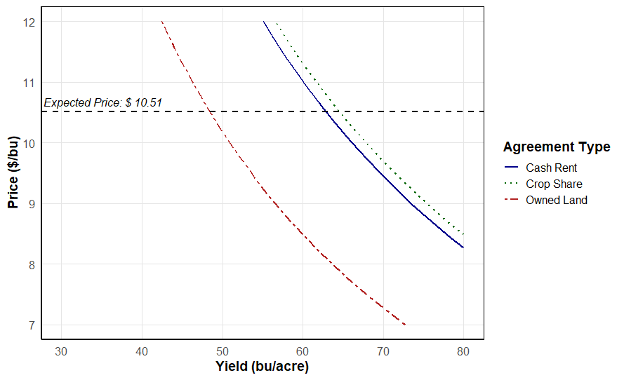

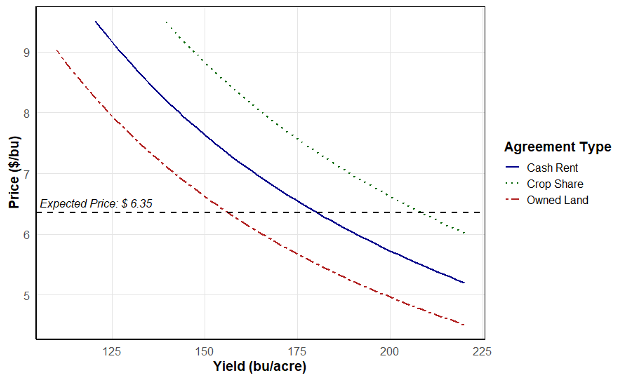

In 2025, U.S. rice acreage amounted to roughly 2.8 million acres, of which 2.7 million acres were harvested (USDA-NASS, 2026). All rice class acreage was down about 4 percent from 2024, due in part to the generational flood event that took place in April across the Midsouth, which forced many farmers to replant, or in some cases leave ground fallow due to razor-thin margins for rice in the South (Biram et al., 2025). Compared to 2025, the upcoming growing season preview shows tighter stocks, with a declining price environment. The January 2026 WASDE report currently pegs long grain ending stocks at about 34.6 million bushels, little changed from the 24/25 marketing year but with a significant change in average farm price, which is currently forecasted at $10.50/cwt (down from $14.00/cwt during the 24/25 marketing year) (USDA, 2026).

2026 International Trade Outlook

International rice prices remain low due to large exportable surpluses, particularly from Asian exporters, and lower import demand from Indonesia. Temporary price increases, such as those observed in Thailand in late 2025, have already reversed, and export prices across major suppliers—including the United States, Uruguay, Thailand, and Vietnam—show sharp year-on-year declines (FAO, 2026). Unless major production shocks occur in Asia, prices are expected to remain depressed through 2026.

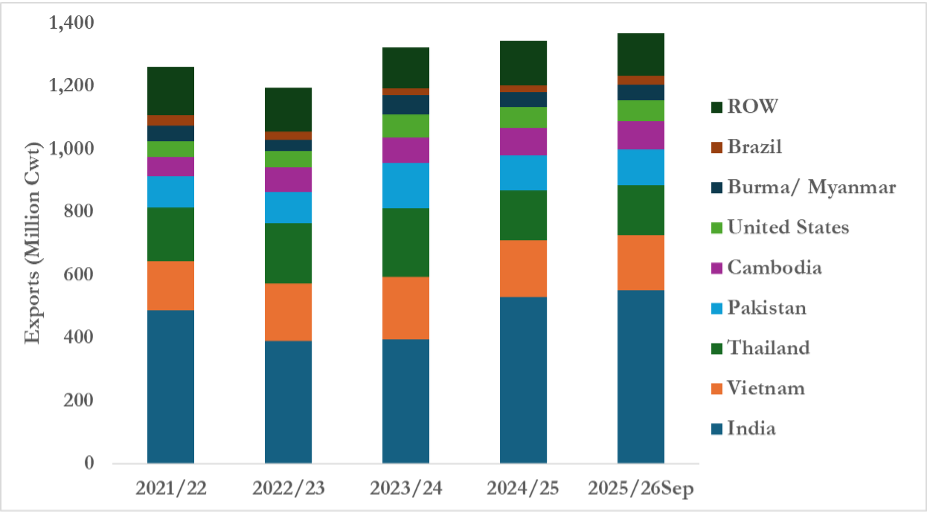

Global rice production for the 2025/26 campaign is projected to be near record levels (around 541 million metric tons), with demand slightly lower (538.6 million metric tons), resulting in a third consecutive year of global surplus and continued stock accumulation (USDA-FAS, 2026). India has emerged as the world’s leading rice producer, surpassing China since 2024/25, and it is expected to reach a new production record in 2025/26 (preliminary reports suggest a record high main Kharif crop harvested in 2025 and an increase in area planted of the second Rabi crop). Its rapidly growing exportable surplus makes India a decisive force in shaping global market dynamics.

Since U.S. long-grain rice competes strongly with Mercosur rice in the Western Hemisphere, it is important to highlight that the upcoming 2025/26 Mercosur harvest is expected to be smaller due to reduced planted area and climatic challenges, although high initial stocks—especially in Brazil—will partially offset lower output (USDA-FAS, 2026). Thus, Mercosur’s lower production performance may be good news for U.S. rice, maintaining or reclaiming market share throughout the Western Hemisphere.

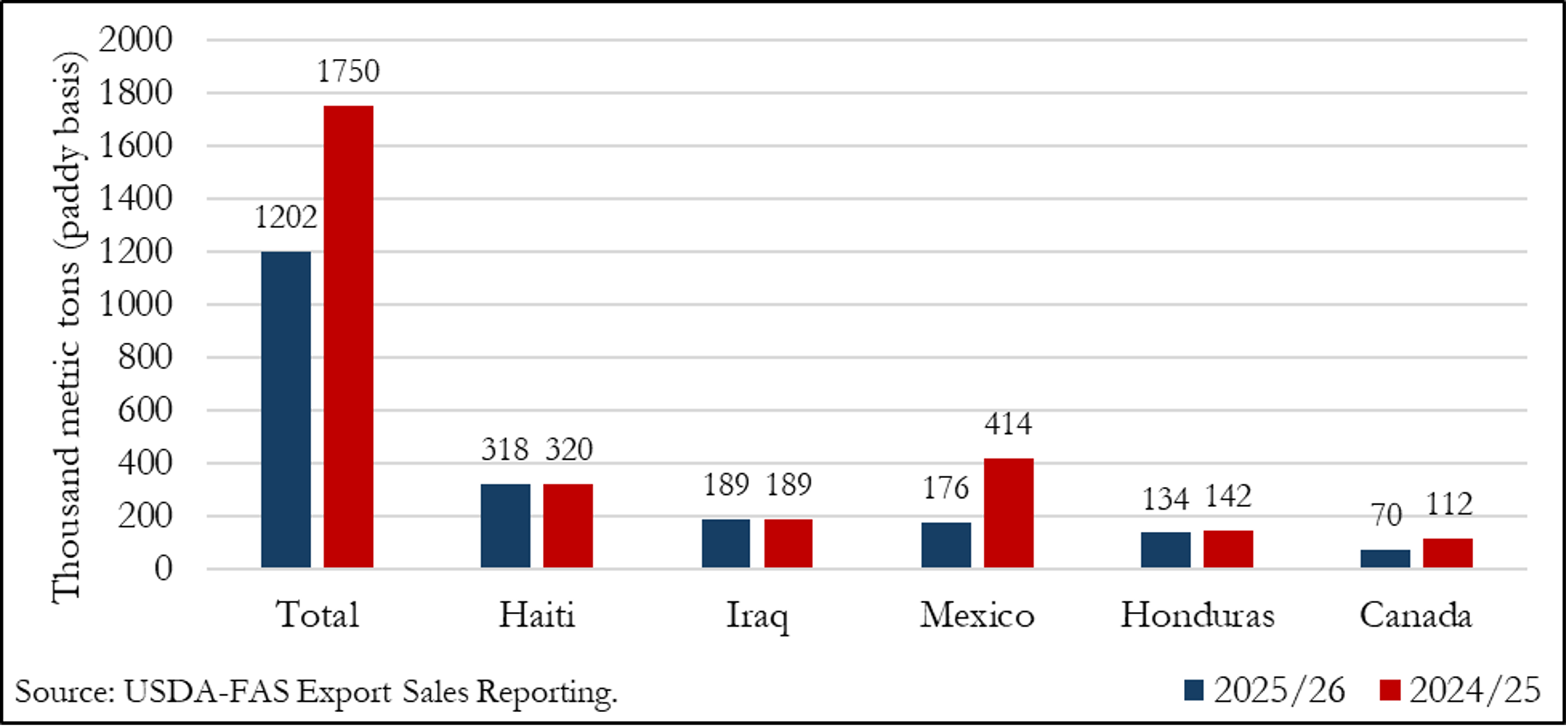

In this international context, U.S. long-grain exports in the first half of marketing year 2025/26 (August-January) decreased 31% relative to the same period a year ago (Figure 1). While the U.S. has maintained export levels to Haiti and Iraq, it has experienced a significant drop in exports to Mexico and, to a lesser extent, to Canada and Honduras, due largely to increasing competition from South America.

Figure 1. U.S. long-grain exports during August-January of the marketing year – total and by top five destinations.

References

Biram, H.D., Loy, R., Hardke, J., Kelley, J., Ross, J., and Davis, J. 2025. Analysis Suggests Historic Flooding Results in $99 Million in Crop-Related Damages. University of Arkansas Factsheet. FSA93. Available online at, https://uaex.uada.edu/publications/PDF/FSA93.pdf.

United States Department of Agriculture, National Agricultural Statistics Service. 2026. Crop Production: 2025 Summary. Available online at, https://esmis.nal.usda.gov/sites/default/release-files/795725/cropan26.pdf.

United States Department of Agriculture. 2026. World Agricultural Supply and Demand Estimates. Available online at, https://www.usda.gov/oce/commodity/wasde/wasde0126.pdf.

FAO Rice Price Update. Available online at https://www.fao.org/markets-and-trade/commodities/rice/fao-rice-price-update/en/

United States Department of Agriculture, Foreign Agricultural Service. 2026. Production, Supply and Distribution Online. Available at https://apps.fas.usda.gov/psdonline/app/index.html#/app/advQuery

United States Department of Agriculture, Foreign Agricultural Service. 2026. Export Sales Reporting. Available at https://apps.fas.usda.gov/esrquery/esrq.aspx

Loy, Ryan, and Alvaro Durand-Morat. “2026 Rice Market Outlook.” Southern Ag Today 6(8.3). February 18, 2026. Permalink