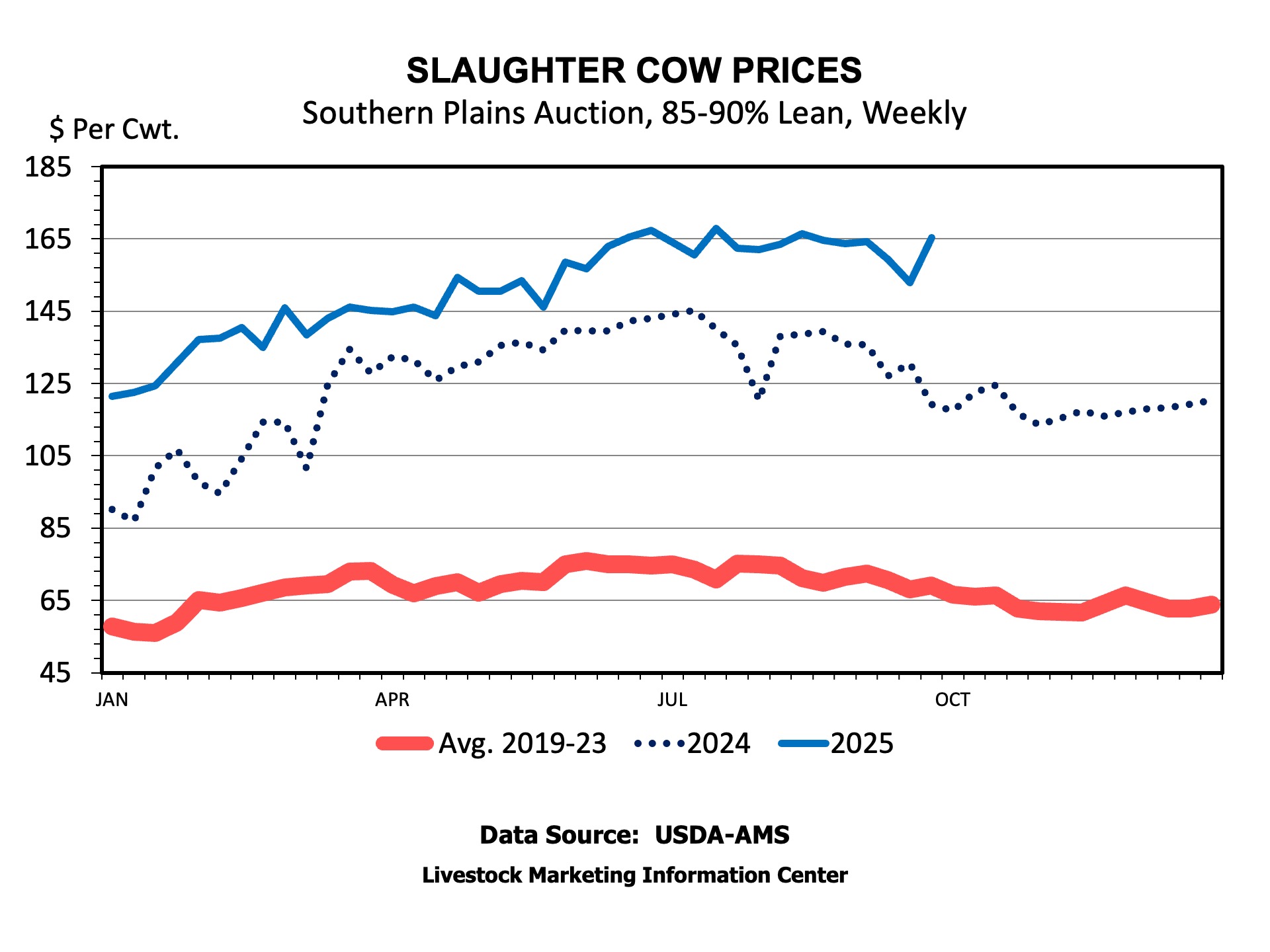

Cull cow prices typically decline this time of the year as beef and dairy cow culling ramp up and the beef market is fully past grilling season. Cow prices this Fall have shown just a little seasonal decline as tight beef supplies keep prices high.

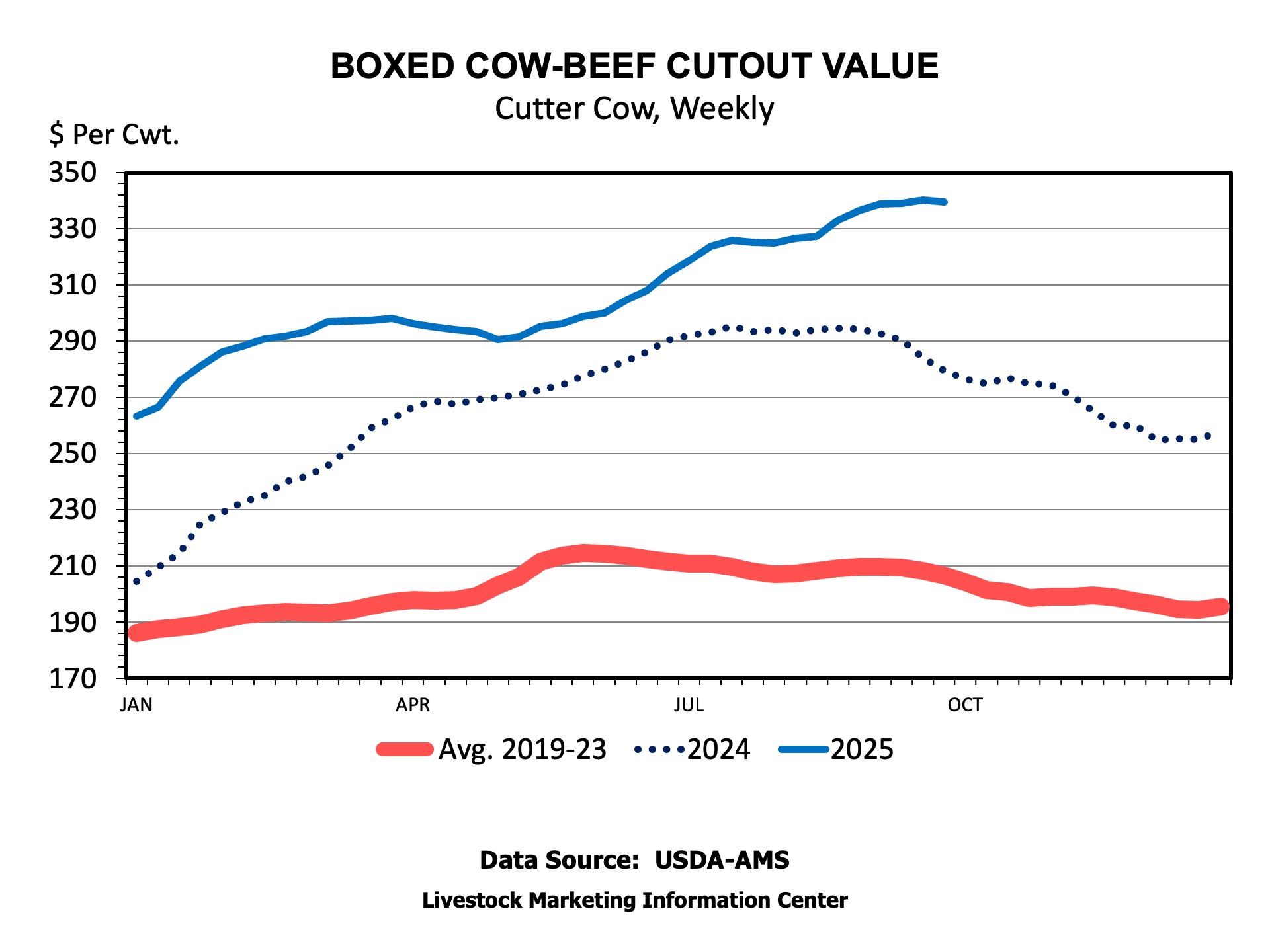

Southern Plains cow prices at auctions have been about $165 per cwt since mid-year, with a brief dip into the low $150s in the last 2 weeks. Prices a year ago at this time were under $120 per cwt. and were declining to their Fall lows. Cutter quality cows have declined from about $137 to about $129 per cwt over the last few weeks, showing a little more seasonal decline. On the meat side, the boxed cow beef cutout and 90 percent lean boneless beef have shown little seasonal decline and are sitting at record levels.

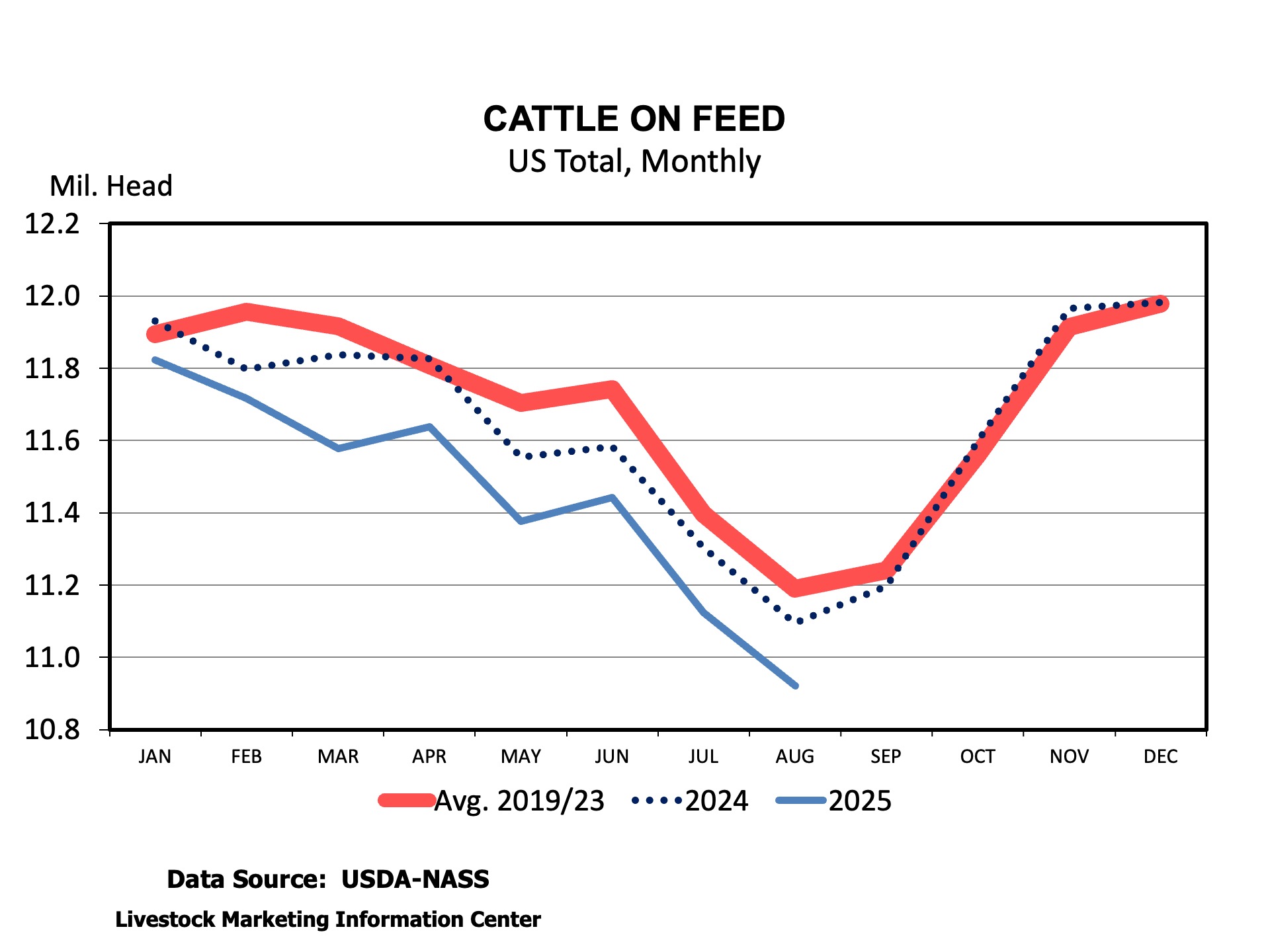

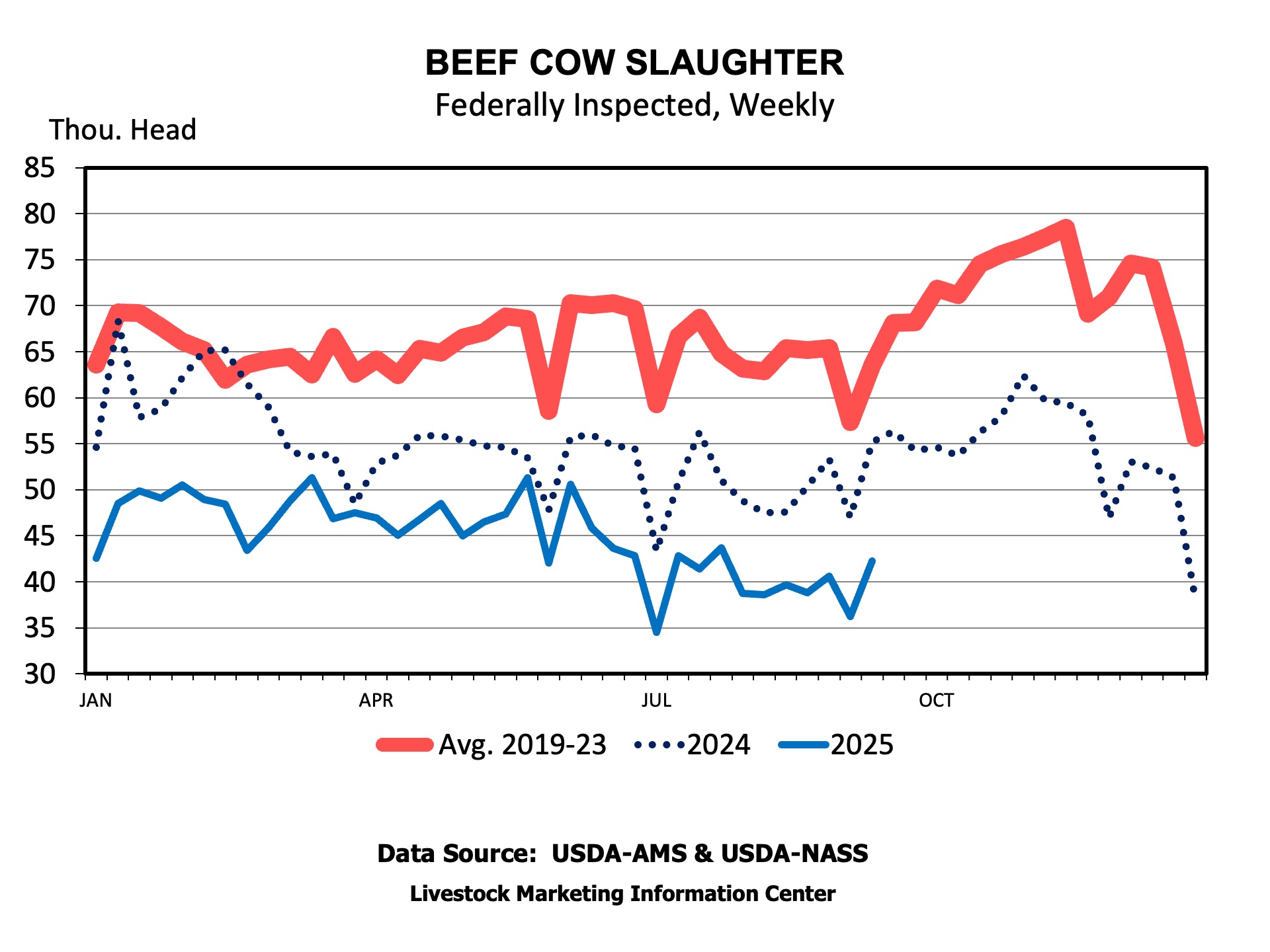

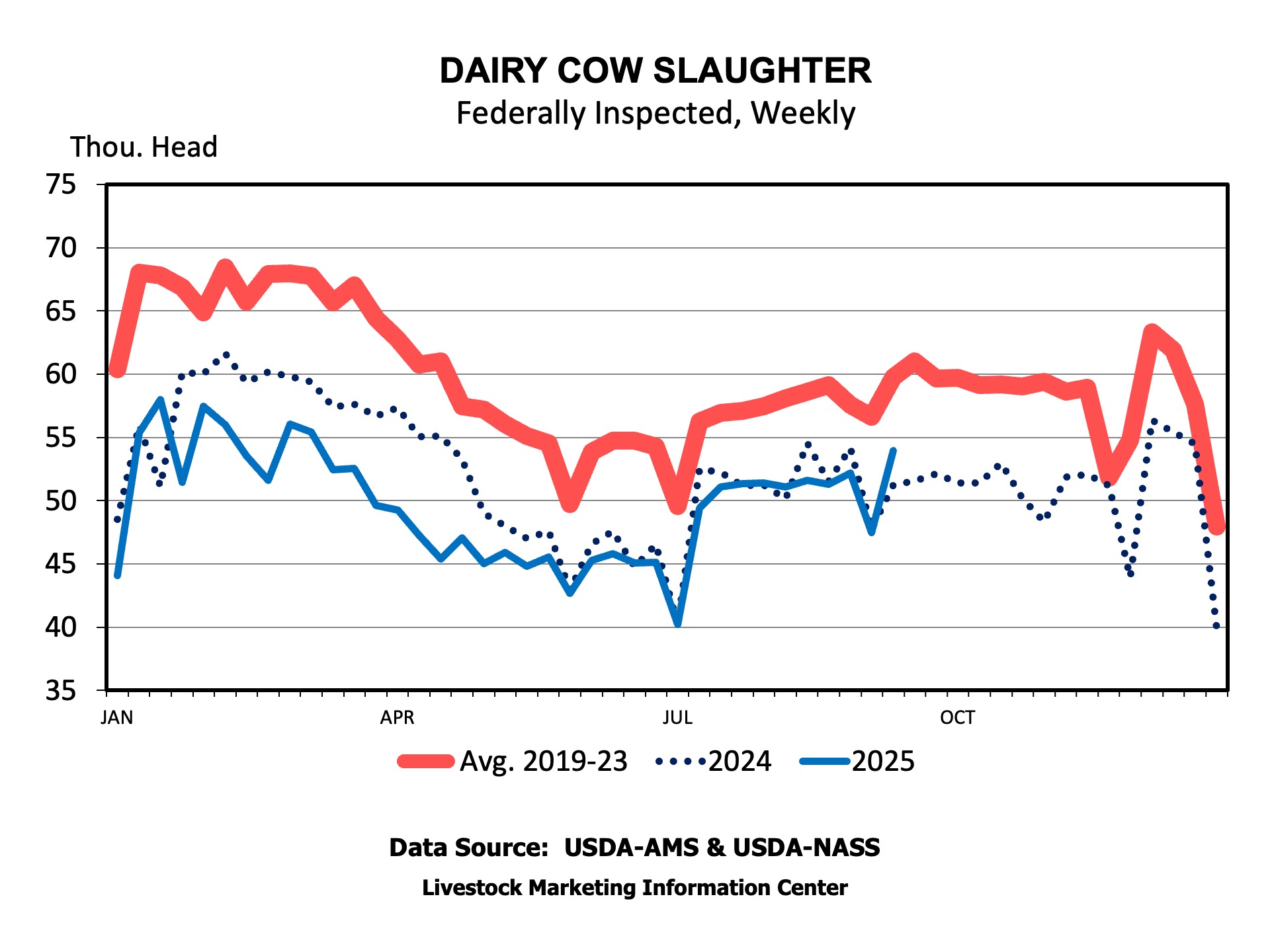

Total cow slaughter includes dairy and beef cows. Beef and dairy cow slaughter each exhibit a different seasonality based on production patterns. Beef cow slaughter hits its peak in the Fall when most culling occurs around the country. Dairy cow slaughter peaks early in the first quarter of the year but, does increase in the Fall. The dairy herd has been expanding this year due to profits hitting over 9.5 million head on September 1, 2025, the most since 1993. As the herd has grown, culling has increased. For the year, total dairy cow slaughter is almost 19 percent smaller than the same period in 2024. But, in the last 2 months dairy cow slaughter is equal to last year. Beef cow slaughter remains well below last year but may begin to pick up seasonally in coming weeks. In total, cow culling has closed the gap compared to last year in recent weeks but, it has not been enough to weaken prices.

Cull cow prices are going to stay high. While a little more beef cow culling should occur this Fall even with larger dairy cow culling it won’t be enough to drastically boost supplies. There is little evidence of consumers switching to competing meats indicating that demand remains quite good. So, overall, this should be the best Fall cull cow market ever.

Anderson, David. “Cull Cow Prices See Just a Little Seasonal Decline.” Southern Ag Today 5(41.2). October 7, 2025. Permalink