Spring weather in the southeast can indeed be a mixed bag. Environmental control systems are strained as poultry growers in the southeastern United States can easily see temperature swings approaching 60 degrees Fahrenheit over 48 hours. While most modern houses today are capable of successfully handling such temperature swings and keeping the birds inside comfortable, the growers themselves feel the strain in the form of utility costs. Historically, the two largest variable costs contract growers must contend with are heating fuel used to keep birds warm and electricity used to keep birds cool. Luckily, falling propane and natural gas prices accompanied the latest cold snap. A relatively mild winter across the US and Europe facilitated this, leading to decreased usage. The results are increasing stocks of propane in the US starting in November ’22 up to the beginning of March ’23 (Fig 1). Increased supply has led to falling prices for propane. Comparing the previous year’s weak supply numbers to the current strong supply situation could indicate that the upcoming winter may also be met with lower heating fuel prices. This is good news for growers heating chicken houses in the U.S. this spring. This could of course change quickly if the winter of ’23 shapes up to be harsh, or if the crude oil prices again rise to higher levels (as propane is closely tied to crude oil production and price.) Even so, going into next winter with a strong supply of propane is a good sign for poultry growers. Natural gas supplies are also predicted to be higher and long-term prices NG are predicted to be down accordingly.

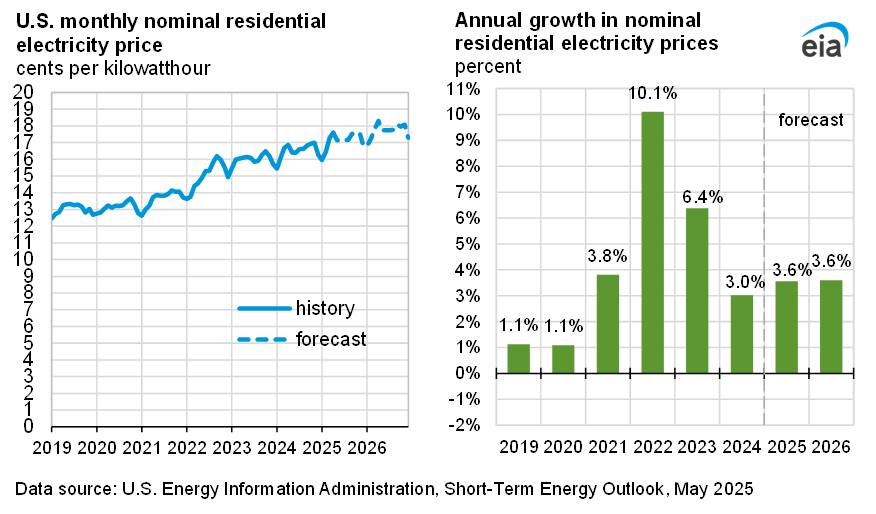

Alternatively, electricity costs are not looking as promising going into the summer when most electricity is used on poultry farms. As poultry houses have become better insulated and better managed to control heating costs, electricity has become the most prevalent cost factor for many growers. Electricity prices saw a significant 10% increase in 2022. While the projection for 2023 is lower at 2.5%, the long-term pricing trend is upward (Fig 2). The causes of this continued increase are varied, from general inflationary forces, increasing demand for electricity met with the increased cost of new generation facilities, to the increased cost for utility companies to implement carbon neutral generation goals. This makes it imperative for growers not only to focus on housing and equipment for heating purposes but also focus on electrical energy usage efficiency. While any money spent on energy efficient upgrades to equipment must be analyzed closely looking at initial cost versus payback over time, electrical efficiency upgrades look to be becoming more and more important going forward.

Figure 1.

Figure 2.

Brothers, Dennis. “Heating Fuel and Electricity Concerns for Commercial Poultry.” Southern Ag Today 3(13.2). March 28, 2023. Permalink

{kind=link}