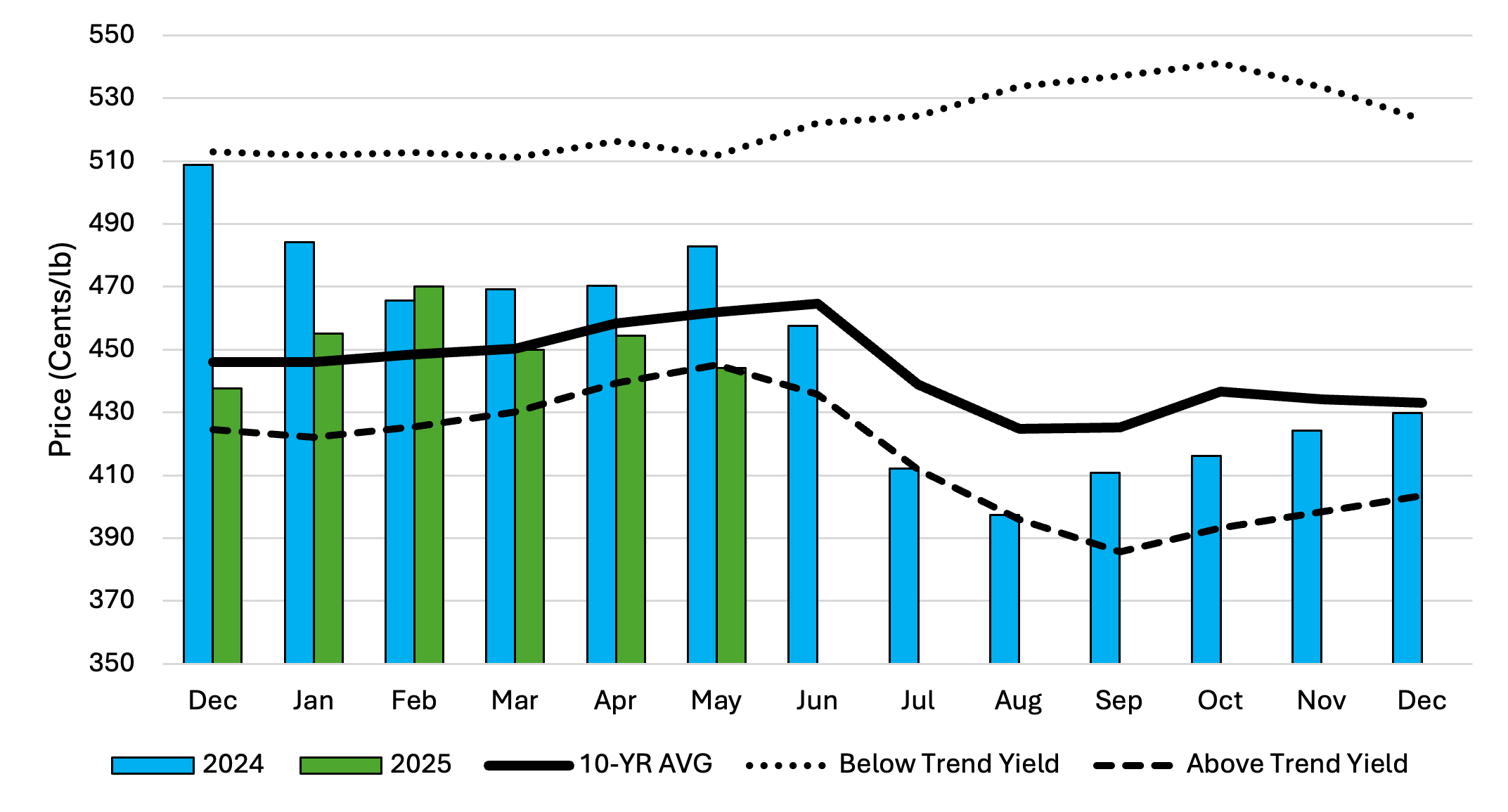

Over the last 2 months, the rapidly changing tariff environment has had livestock market analysts anxiously awaiting USDA trade data releases. The latest monthly trade data from the USDA was published on June 6th. It included meat and livestock exports and imports for April 2025.

Trade is interesting because of all the moving parts. Tariffs are only a part of the story. Domestic production impacts prices, creating incentives to import or export. For example, record high beef prices creates an incentive to import more beef and export less. Relative prices between countries, exchange rates, shipping costs and availability, and other countries’ actions may impact trade, overwhelming the effect of a new tariff.

U.S. companies exported 237 million pounds of beef in April, an 18.5 million pound decline from March and 22.3 million pounds less than April 2024. Exports to China declined the most, down 27.7 million pounds, or 34 percent, compared to March. The impact of China on total U.S. beef exports was partially offset by larger exports to Japan, South Korea, and Hong Kong. It’s not unusual for beef exports to decline from March to April. On the pork side, exports declined 58 million pounds, or 9 percent, from March, and 73 million pounds less than April 2024. Shipments to most markets declined, led by Canada, Mexico, and China. The decline in pork exports to Canada accounted for 41 percent of the total export reduction from March.

Beef imports declined in April compared to March, down 27 million pounds. As with exports, it’s normal for imports to decline from March to April. Fewer imports came from Canada, Mexico, New Zealand, and Uruguay. Imports jumped 17.8 million pounds, 17 percent, from Brazil. The increase in imports from Brazil bucked the usual trend of declining imports after January.

Lamb imports have been a very contentious issue for the industry for many years. The imposition of tariffs on Australian and New Zealand imports, which make up 99 percent of U.S. lamb imports, has had industry backers and detractors. Imports in April were 5 percent larger than those in March and 10 percent larger than those in April 2024. Some other factors are clearly at work in the lamb market, and it may take more time to see any impacts of tariffs that were imposed in early April.

The April trade data gives us an early glimpse at the impacts of tariffs on meat trade. The May data may give us a better look at impacts because that will better account for shipping time lags for some markets. Clearly, the very large tariffs between the U.S. and China did impact that transaction. Other markets with smaller tariff levels may not reveal large changes yet.

Anderson, David. “A Little More Insight on Meat Trade.” Southern Ag Today 5(24.2). June 10, 2025. Permalink